All Categories

Featured

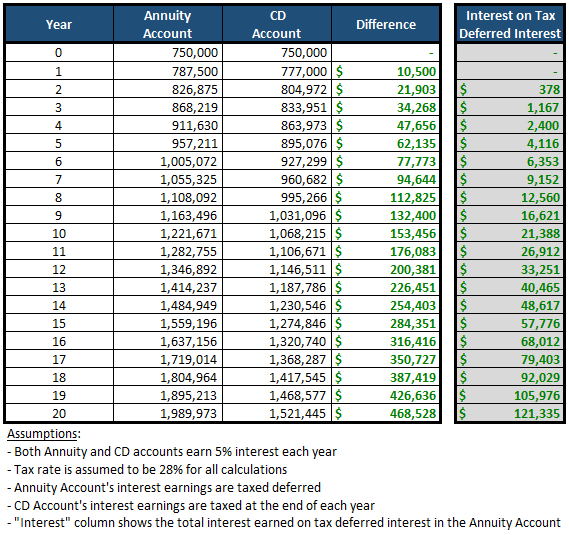

The finest choice for any individual must be based upon their current scenarios, tax scenario, and financial objectives. Flexible premium annuities. The cash from an inherited annuity can be paid out as a solitary round figure, which ends up being taxable in the year it is gotten - Annuity contracts. The disadvantage to this option is that the profits in the contract are distributed first, which are tired as common revenue

If you do not have an instant requirement for the cash money from an inherited annuity, you can choose to roll it into another annuity you regulate. With a 1035 exchange, you can guide the life insurance provider to move the money from your inherited annuity right into a brand-new annuity you establish. If the acquired annuity was initially established inside an IRA, you might exchange it for a qualified annuity inside your own IRA.

Nonetheless, it is normally best to do so as soon as feasible. This will make certain that the payments are received without delay which any problems can be handled promptly. Annuity recipients can be disputed under specific situations, such as disagreements over the credibility of the beneficiary classification or insurance claims of unnecessary impact. Consult lawful specialists for assistance

in contested recipient scenarios (Retirement annuities). An annuity survivor benefit pays a set amount to your recipients when you pass away. This is different from life insurance policy, which pays out a fatality benefit based on the stated value of your policy. With an annuity, you are essentially buying your own life, and the death advantage is meant to cover any exceptional prices or debts you might have. Beneficiaries get payments for the term defined in the annuity agreement, which can be a set period or permanently. The duration for paying in an annuity differs, yet it often drops in between 1 and 10 years, depending upon agreement terms and state legislations. If a beneficiary is incapacitated, a legal guardian or a person with power of lawyer will manage and obtain the annuity settlements on their behalf. Joint and recipient annuities are the two kinds of annuities that can prevent probate.

{kind=link}

Latest Posts

Decoding How Investment Plans Work A Comprehensive Guide to Investment Choices Defining Fixed Index Annuity Vs Variable Annuity Benefits of Fixed Annuity Vs Variable Annuity Why Choosing the Right Fin

Analyzing Fixed Vs Variable Annuity Everything You Need to Know About Pros And Cons Of Fixed Annuity And Variable Annuity Breaking Down the Basics of Investment Plans Features of Choosing Between Fixe

Decoding How Investment Plans Work A Comprehensive Guide to Investment Choices Defining Fixed Income Annuity Vs Variable Annuity Pros and Cons of Various Financial Options Why Choosing the Right Finan

More

Latest Posts